Since the “great recession,” interest rates have been considered low by historical standards, and it’s not just a recent phenomenon. Real interest rates and inflation have been in decline since the 1980s. While this trend has been a potential boon to borrowers, it’s been a source of irritation to savers and retirees trying to live on the income from their investment portfolios.

What’s an investor to do? For some, the temptation to chase yield is strong. Dividend-paying stocks offer more attractive yields. But the attraction can be illusory. Investors should focus on total returns rather than dividends.

Dividend Irrelevance

Research by Nobel Prize winners Merton Miller and Franco Modigliani showed that dividend policy should have no effect on stock prices or expected returns in perfect capital markets.1 If a stock’s dividend is too low to meet income needs, an investor can sell some shares to create a “homemade dividend.” Likewise, if a stock’s dividend is too high, investors can use some of the dividend to buy more shares. Since its publication in 1961, the Miller-Modigliani “dividend irrelevance theorem” has framed the debate on dividend policy.

Dividend irrelevance is an elegant theory, but does it hold up in practice? Let’s take a look at the historical record. I examined monthly returns on U.S. stocks for the period July 1927 to October 2016, looking at four investment strategies:

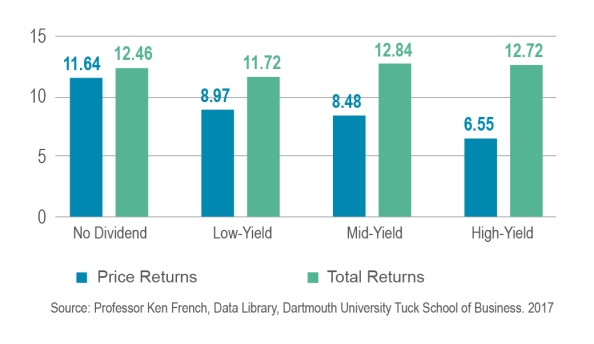

- No-dividend stocks

- Low-yield stocks

- Mid-yield stocks

- High-yield stocks

Each strategy is represented by a portfolio that is rebalanced once per year. Each July, individual stocks are sorted into one of four equally-weighted portfolios based on their dividend yield at the end of the previous December.

The figure below plots annualized average total and price returns for the four strategies. Total returns are the sum of price returns and income returns. As you can see, high-yield stocks earn the same total return, on average, as low-yield or non-dividend-paying stocks. This is consistent with the Miller-Modigliani theoretical prediction that dividend policy is irrelevant.

The average price returns are higher for portfolios with lower-dividend yields. This is expected, but not meaningful. The owners of low-yield stocks receive their returns in the form of higher capital appreciation, on average, to make up for the lower average income returns.

We construct our model portfolios based on the risk and expected total return of asset classes. As suggested by theory, we do not chase dividend yield. Tilting toward dividend-paying stocks may increase portfolio risk (by reducing the benefits of diversification) without potentially offering any improvement in portfolio expected return. Periodically redeeming fund shares to provide income is a perfectly natural part of retired life. Financial advisors can help investors with these decisions.

1Miller, M., & Modigliani, F., 1961, “Dividend Policy, Growth, and the Valuation of Shares.” The Journal of Business 34, 411-433. In theory, assuming perfect capital markets implies no transaction costs, no taxes, and no information costs.