In the last two weeks, despite geopolitical tensions around Iran, financial markets have shown resilience with stock indexes hitting new records and positive signals from major U.S. bank earnings. Inflation concerns continue as consumer prices surged in March, while defense spending debates and energy sector developments add complexity to the economic landscape. Let’s dive in!

- Market Resilience: Despite Middle East conflict and economic risks, U.S. stocks reached record highs as investors anticipate a near-term resolution and sustained tech-driven growth. Analysts caution that prolonged war could trigger market corrections, underscoring the value of a long-term investment approach.

- Bank Earnings Surge: Major US banks reported a 12% profit increase in Q1, driven by strong consumer spending and resilient economic conditions, despite geopolitical and market uncertainties. Trading revenue and dealmaking fees also saw significant growth.

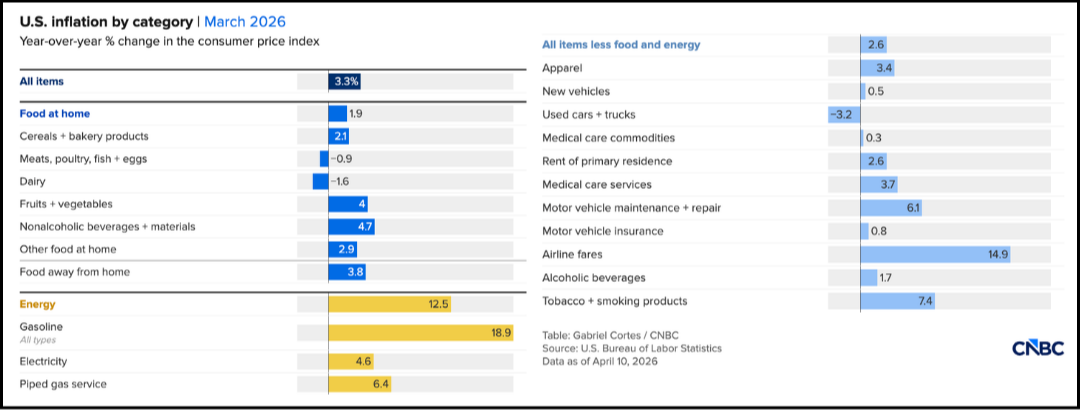

- Inflation Surge: U.S. consumer prices rose 0.9% in March, the largest increase in nearly four years, driven by higher oil prices from the Iran conflict and tariff effects. Excluding volatile food and energy, core CPI increased 0.2%, signaling sustained inflation pressures and diminishing chances for rate cuts this year.

- Private Credit Outlook: PIMCO and Wall Street leaders agree the $3.5 trillion private credit market does not pose systemic risks, citing contained defaults and limited leverage. Experts believe that current conditions differ from the 2008 crisis, with stronger safeguards reducing financial stability concerns.

- Mortgage Lock-In: More than half of mortgages still have rates below 4%, causing homeowners to stay put amid higher current rates around 6.4%. This lock-in effect limits housing supply, suppresses sales, and keeps home prices elevated, with rate relief needed to prompt more seller activity.

- Strait of Hormuz: Iran initially announced that commercial passage through the Strait of Hormuz would remain open during a 10-day ceasefire, easing tensions and triggering a market rally with crude oil prices dropping over 10%. However, the strait has since been closed again amid renewed conflict, underscoring its ongoing instability and the risk of further disruptions to global energy markets.

- Defense Spending Trade-Off: The IMF highlights a global rise in military budgets, warning this may increase public debt and reduce social spending. While some governments see defense as a jobs driver, escalating tensions challenge fiscal balances and force tough choices between security and social priorities.

- Gen Z IRA Growth: Gen Z investors now lead IRA contributions, accounting for 34% of total contributions in 2025, with overall IRA contributions up around 30%. This is an encouraging trend, indicating a shift toward proactive retirement planning and early wealth accumulation.

- U.S. Nuclear Reactors: As part of a broader push to expand nuclear energy, the U.S. Energy Department is expected to offer loans for an initial group of 5–10 new reactor projects, aligned with President Donald Trump’s 2030 construction target of 10 reactors. Increased funding and partnerships aim to accelerate progress despite past cost and timing challenges.

Over the next two weeks, investors will be closely watching key U.S. inflation data to better understand how it may influence the Federal Reserve’s path on interest rate cuts. At the same time, developments in the Iran conflict, particularly around any ceasefire progress and stability in the Strait of Hormuz, will be important to monitor given their impact on energy prices and overall market sentiment.

Footnotes

- Why the stock market is hitting records despite Iran war (CNBC)

- A resilient American economy: 3 takeaways from big bank earnings (Yahoo Finance)

- Wall Street indexes rally after Iran says Strait of Hormuz completely open (Reuters)

- Private credit is not a systemic risk, PIMCOs Ivascyn says (Investing.com)

- COVID-era homeowners are still hanging on to their ultra-low-rate mortgages (Yahoo Finance)

- US consumer prices surge as expected in March (Investing.com)

- Guns vs. butter: IMF flags tough trade-offs as governments ramp up defense spending (CNBC)

- Gen Z is driving IRA contributions to record highs. Heres how to get started. (Yahoo Personal Finance)

- First new planned US nuclear reactors likely to get government loans, energy chief says (Investing.com)